A truck carrying spices from Kerala to Delhi is stopped at a check-post in Andhra Pradesh. The driver has everything the law demands: tax invoices, e-way bills, every document prescribed under Section 68 of the CGST Act. The goods are perishable. The consignment is an interstate supply, taxable under the IGST Act. Andhra Pradesh is neither the origin state nor the destination state. It has no fiscal stake in the transaction; not a rupee of the IGST collected on this supply will flow to its exchequer.

Yet the goods are detained. Then confiscated under Section 130. The ground? "Undervaluation." The driver is stranded. The spices begin to deteriorate. And a state that has no constitutional entitlement to any part of the tax on this transaction has effectively held the goods hostage, demanding penalties from a supply chain it has no authority to tax.

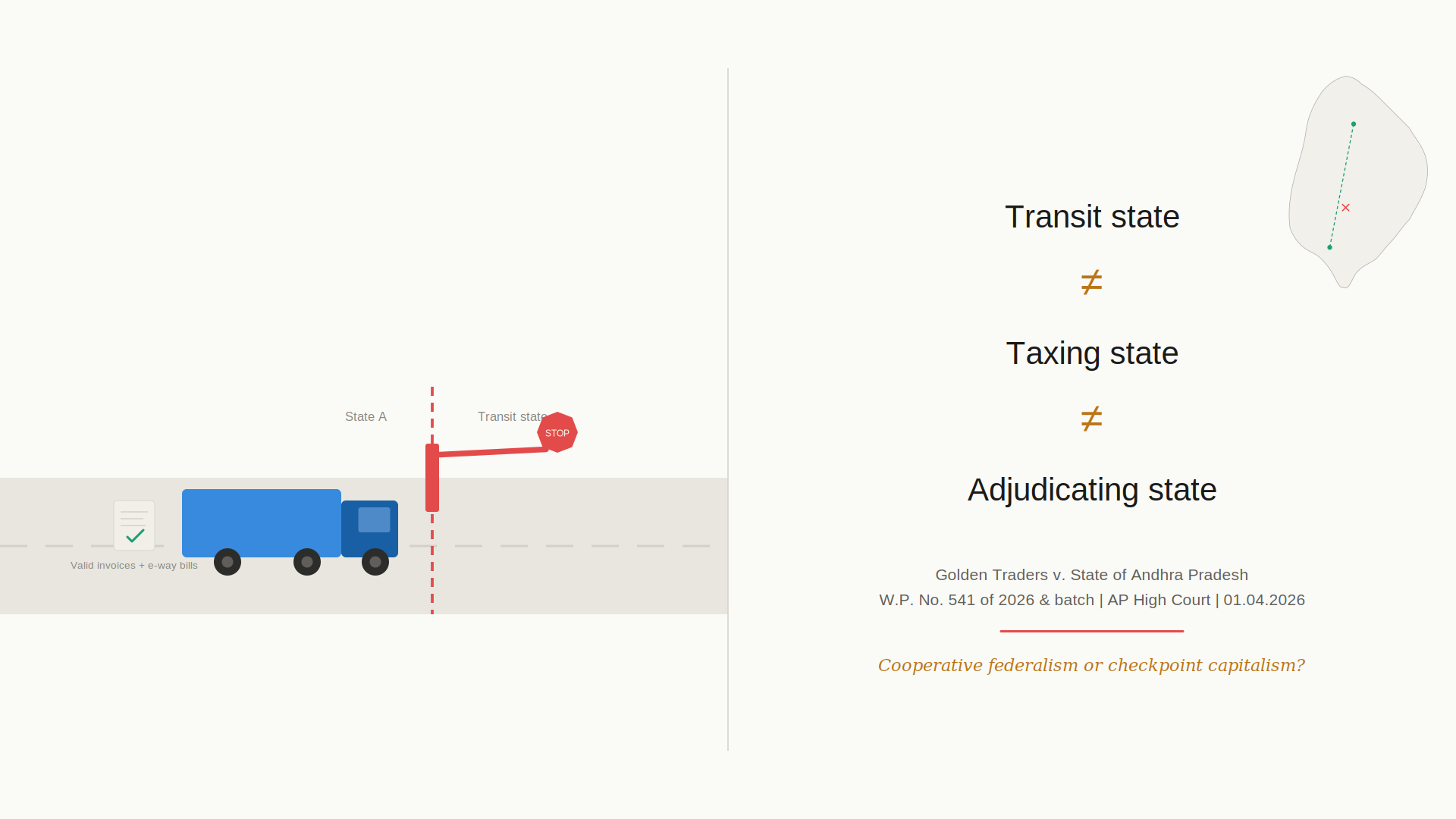

This is not a hypothetical. This is the fact pattern, repeated across nine writ petitions, that came before the Andhra Pradesh High Court in Golden Traders v. State of Andhra Pradesh. And the question it forces us to confront is uncomfortable but necessary: is this cooperative federalism, or is it checkpoint capitalism?

W.P. No. 541 of 2026 and batch | AP High Court | Decided 01.04.2026

Bench: Justice R. Raghunandan Rao and Justice T.C.D. Sekhar

The Constitutional Architecture: One Nation, One Tax

To understand why the AP High Court's ruling matters, you have to start with the constitutional design.

Article 246A of the Constitution, introduced by the 101st Amendment, created a system of simultaneous taxation. Both Parliament and state legislatures can levy GST on the same supply. But Article 246A(2) carves out a critical exception: Parliament has exclusive power to legislate on goods and services tax where the supply takes place in the course of inter-state trade or commerce. This is not a shared power. It is an exclusive central domain.

Article 269A reinforces this architecture. IGST on inter-state supplies is levied and collected by the Government of India. The tax is then apportioned between the Union and the states, but not arbitrarily. Section 17 of the IGST Act prescribes the apportionment mechanism. The state share goes to the state where the supply takes place, which in turn is determined by the place of supply rules. A transit state through which goods merely pass en route from origin to destination receives nothing. Not a fraction of the IGST, not a share of any penalty or fine collected in connection with that IGST transaction.

This is not an accidental gap. It is a deliberate design choice. The GST architecture was built to dismantle the fragmented indirect tax regime that treated every state border as a fiscal checkpoint. The constitutional promise was a seamless national market. Articles 246A and 269A, read with Section 17 of the IGST Act, are the structural pillars of that promise.

Now layer on the cross-empowerment provisions. Section 6 of the CGST Act and Section 4 of the IGST Act authorize state tax officers to function as "proper officers" under the central and integrated GST statutes. But this cross-empowerment was designed to solve a specific problem: preventing duplication of proceedings where a taxpayer is administratively allotted to either the Centre or the State. It was not designed to give every state officer in every transit state blanket jurisdiction over every IGST consignment passing through the state's territory. Cross-empowerment is an allocation mechanism. It is not a power-conferring provision untethered from fiscal entitlement.

What the Andhra Pradesh High Court Actually Held

The bench heard nine writ petitions together. The fact pattern was strikingly uniform: goods originating in Kerala or Karnataka, destined for Maharashtra or Delhi, intercepted at check-posts in Andhra Pradesh. In every case except one, the consignments were accompanied by all documents required under Section 68. The grounds for detention and confiscation were undervaluation, quantity mismatch, or description discrepancy, not the absence of documentation.

The Court's analysis proceeded on two tracks: jurisdiction and the permissible scope of Sections 129 and 130.

On jurisdiction, the Court rejected the respondents' argument that Section 6 of the CGST Act and Section 4 of the IGST Act automatically cross-empower any state officer to act as a "proper officer" under the central statutes without limitation. The Court held that cross-empowerment is not self-executing and unlimited. An officer appointed under the APGST Act can function as a "proper officer" under the CGST or IGST Act only in relation to a taxpayer administratively allotted to that state, and only where that officer has been assigned the relevant function by the Chief Commissioner.

The Court noted the Supreme Court's observations in Armour Security (India) Ltd. v. Commr. (CGST), (2025) 145 GSTR 385 : 2025 SCC OnLine SC 1700, which emphasized that Section 6(2) is designed to prevent multiplicity of proceedings and to secure uniformity, not to grant overlapping jurisdictions.

The doctrinal innovation came in the Court's treatment of Sections 129 and 130 under the IGST Act. The Court held that while a state officer exercising Section 129/130 functions can act under the CGST Act for intra-state supplies, the position is different for IGST. A state officer can exercise Section 129/130 powers under the IGST Act only when the state is entitled to an allocation of tax under Section 17 of the IGST Act in relation to the specific transaction. Where goods originate outside the state and are destined outside the state, where the state is merely a transit corridor, the state officer has no jurisdiction to detain, seize, or confiscate those goods under IGST.

The Court further endorsed the line of authority from the Kerala High Court in Alfa Group, the Chhattisgarh High Court in K.P. Sugandh Ltd., the Gujarat High Court in Panchi Traders, and the Allahabad High Court in Shambhu Saran Agarwal, holding that undervaluation is not a permissible ground for detention or confiscation under Section 129 or 130.

The five-point holding is worth distilling:

- (A) Cross-empowerment under CGST/IGST requires administrative allotment of the taxpayer to that state

- (B) State officers can exercise Section 129/130 functions under CGST for intra-state supplies

- (C) For IGST, the state must be entitled to a share of tax under Section 17

- (D) A transit state, where goods originate and terminate outside its borders, cannot exercise Section 129/130 powers under IGST

- (E) Discrepancies found in IGST consignments can be forwarded to the proper officers of the consignor and consignee for further action

The Revenue Arbitrage Problem

This is where the implications need to be stated plainly.

What transit states are doing at check-posts is not enforcement. It is revenue arbitrage. They intercept IGST consignments in which they have no fiscal stake. They invoke Section 129 or Section 130, provisions designed for genuine evasion, on grounds like "undervaluation" that no High Court has accepted as a valid basis for roadside detention. They levy penalties, collect fines, or confiscate goods. And they appropriate every rupee collected from transactions in which the Constitution gives them no entitlement.

Section 17(3) of the IGST Act provides that penalties collected in connection with an IGST transaction are supposed to be apportioned between the Union and the destination state, not the transit state. But when a transit state officer collects a fine under Section 130, there is no operational mechanism to reapportion that amount to the states actually entitled to it. The transit state simply keeps it.

This is a cooperative federalism problem of the first order. The GST Council designed a system premised on shared sovereignty, coordinated administration, and trust between taxing jurisdictions. Check-post officers in transit states are operating as if state borders are fiscal borders, precisely the pre-GST fragmentation that the 101st Amendment was meant to eliminate. If left unchecked, the risk is the incremental recreation of the octroi-and-checkpoint regime that GST was supposed to dismantle. One truck, one check-post, one confiscation order at a time.

The Enforcement Gap: Doctrine vs. Highway

The Court was pragmatic about one thing. It acknowledged that an intercepting officer at a check-post will not know, at the moment of stopping a vehicle, whether the consignment is an IGST supply or an intra-state supply. The officer has to stop the vehicle and verify the documents before the jurisdictional question can be answered. The Court carved out a sensible protocol: if verification reveals that the consignment is an inter-state supply transiting through the state, the officer must release the vehicle and, if discrepancies are found, forward the information to the proper officers at the origin and destination.

This is doctrinally sound. It balances enforcement needs against jurisdictional limits. But will it work on the ground?

The reality is that check-post operations are driven by revenue targets, not jurisdictional nuance. Officers at state borders are incentivized to detain, not to release. The protocol the Court has laid down requires institutional culture change, training, accountability, and a willingness to let goods pass when the state has no skin in the game. Judgments bind. But they have to reach the check-post to matter. And in the gap between doctrine and highway, goods will continue to rot, drivers will continue to wait, and traders will continue to pay penalties they do not owe, to states that have no right to collect them.

The Question That Lingers

The Andhra Pradesh High Court has drawn the jurisdictional line with clarity and constitutional precision. Transit State ≠ Taxing State ≠ Adjudicating State. That principle is now part of the law.

But a High Court judgment, however well-reasoned, operates within its territorial jurisdiction. The deeper question is whether the GST Council will institutionalize this principle at a national level, through a binding circular clarifying that transit states cannot invoke Sections 129 and 130 for IGST consignments, through an amendment to those provisions explicitly excluding transit-state jurisdiction, or through a standardized forwarding protocol that channels discrepancies to the proper officers at origin and destination.

Until that happens, trucks will continue to be stopped, goods will continue to deteriorate, and the promise of "One Nation, One Tax" will remain, for too many traders on too many highways, a slogan rather than a system.